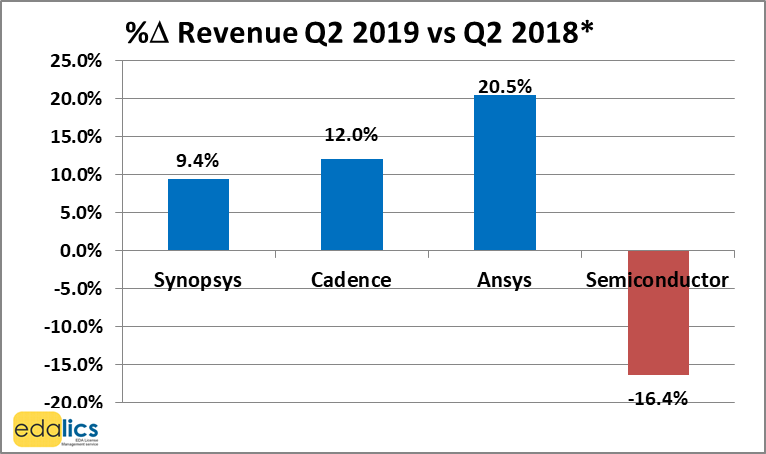

Global semiconductor revenues dropped by 16.4% to $98.6billion in Q2 2019 vs. Q2 2018 (WSTS), while Q1 2019 was also a 13% decline vs. Q1 2018. Gartner is forecasting a 9.6% decrease in 2019 semiconductor revenue to $429 billion, from $475 billion in 2018.

Despite this declining trend headwind in semiconductor revenues, revenues in the EDA market continued to grow steadily, with Synopsys growing quarterly revenues by 9.4% Q2* 2019 vs Q2* 2018 to $853M, while Cadence reported double digit 12% growth to $580.4M and Ansys grew its quarterly revenues fastest by 20.5% Q2* 2019 vs Q2* 2018 to $368.6M:

For comparison, the % growth rates in the previous quarter, Q1* 2019 versus Q1* 2018 were Synopsys 7.7%, Cadence 11.5%, Ansys 12.1%, ESD Alliance 12.9% and Semiconductor -13.0%.

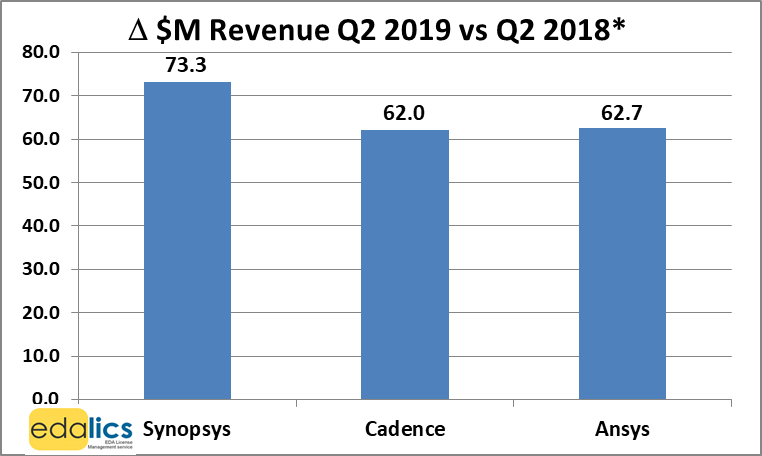

Examining the delta in revenue growth in dollars, Synopsys, Cadence and Ansys’ Q2* 2019 vs Q2* 2018 revenues increased by $73.3M, $62.0 and $62.7 Million respectively, surpassing their prior mid-point guidance by $20.0M, $0.4M and $35.7M respectively:

Guidance for the next quarter and year

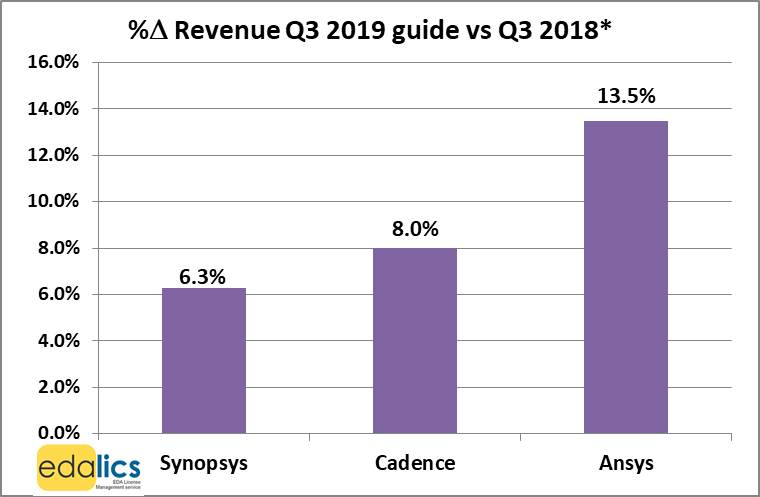

The headwinds of declining Semiconductor revenues are not impacting the EDA companies’ own mid-point guidance either, which is for revenue growth as follows in Q3* 2019:

• Synopsys: 6.3% ($49.9M growth to $845M under ASC 606 rules)

• Cadence 8.0% growth ($42.5M growth to $575M under ASC 606 rules)

• Ansys 13.5% growth ($39.0M growth to $328M under ASC 606 rules)

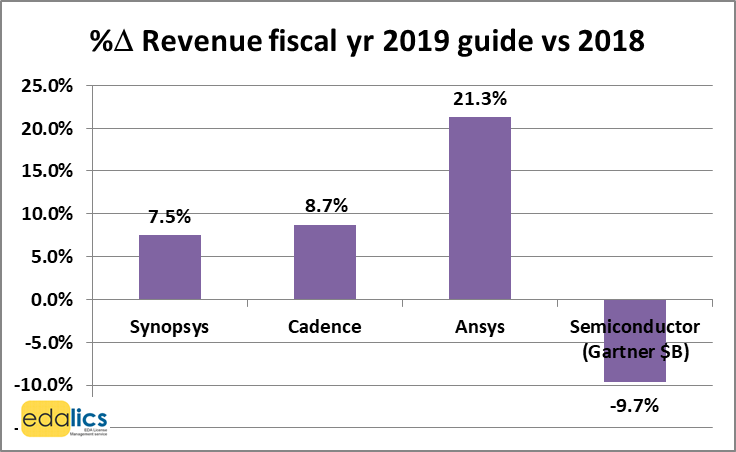

The full (fiscal) year 2019 growth forecasts are: Synopsys 7.5%, Cadence 8.7%, Ansys 21.3% and Semiconductor to decline by 9.7% (Gartner forecast), which confirms that the divergence in revenue trends between EDA and Semiconductor is not merely for just one or two quarters:

In summary, global semiconductor revenue dropped by 16.4% to $98.6 billion in Q2 2019 vs. Q2 2018 (SIA), while Synopsys revenues grew by 9.4%, Cadence by 12.0% and Ansys by 20.5%. The EDA companies own guidance for Q3* 2019 is for slower growth rates: Synopsys to grow revenues by 6.3%, Cadence by 8.0% and Ansys by 13.5%, still growing significantly despite the backdrop of declining Semiconductor revenues.

The author, Gerry Byrne, is the founder of edalics, the niche consultancy which benchmarks and reduces EDA budget costs for leading semiconductor companies.

* Based on each company’s reported financial quarterly data which most closely match that calendar quarter.